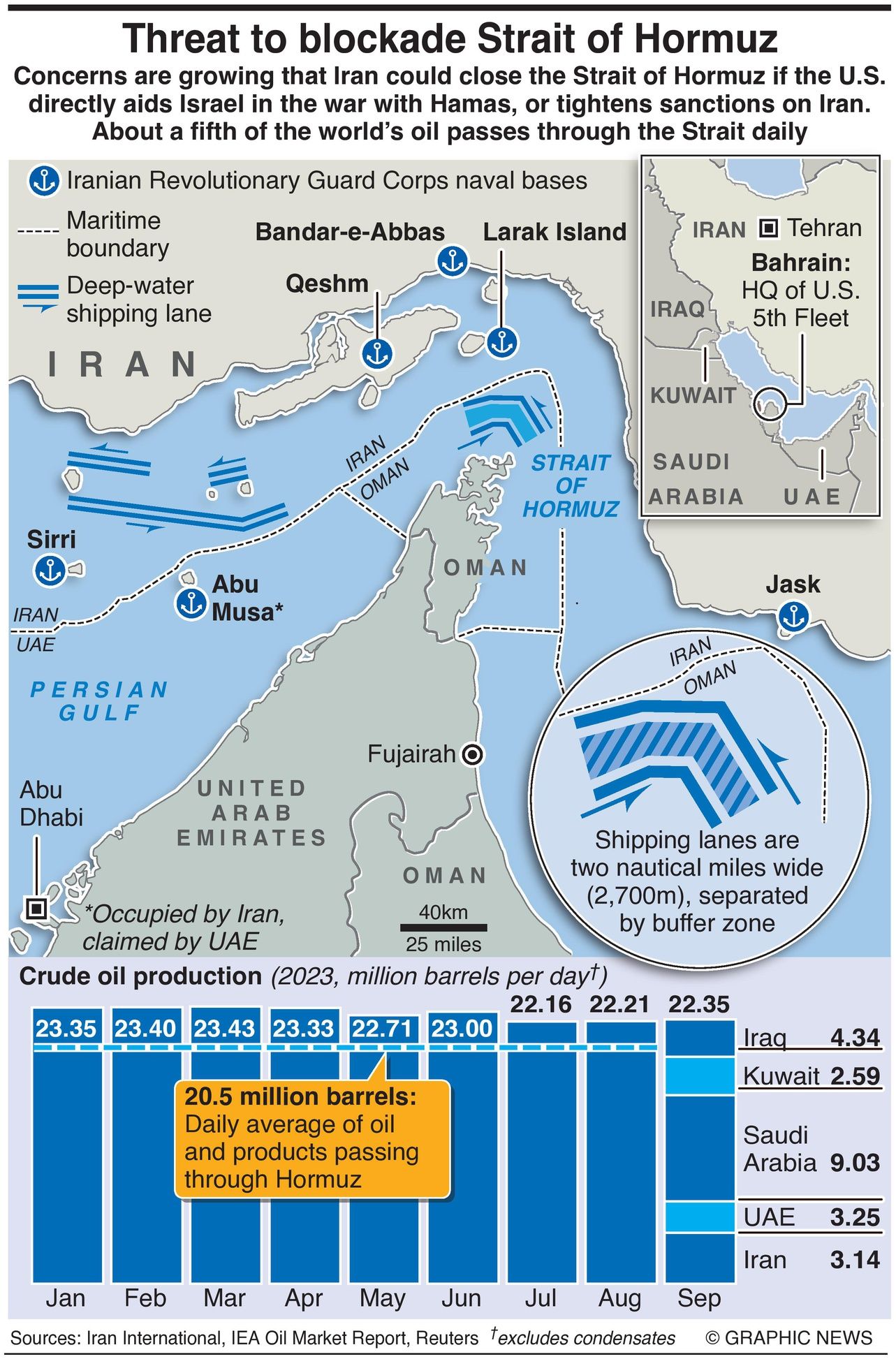

The global maritime logistics network is currently navigating a "dual blockade" architecture—a phenomenon where both the territorial power (Iran) and the global hegemon (the United States) have simultaneously weaponized the Strait of Hormuz. This is not a standard shipping delay; it is a structural dismantling of the "just-in-time" energy model. As of April 2026, the Strait, which traditionally facilitates the passage of 20.9 million barrels of oil per day (b/d), has seen transit volume collapse by approximately 75%.

The crisis is defined by a feedback loop of kinetic warfare, prohibitive insurance premiums, and the total failure of maritime deterrence. To understand the depth of this crisis, one must look past the headlines and analyze the three specific mechanisms driving the current paralysis.

The Triad of Maritime Paralysis

The closure of the Strait is not merely a physical obstruction; it is a three-layered economic constraint.

1. The Insurance Risk Premium Escalation

The primary bottleneck for global shipping is no longer the physical presence of naval vessels, but the actuarial impossibility of securing Hull and Machinery (H&M) and Protection and Indemnity (P&I) coverage. Since the initiation of Operation Epic Fury in February 2026, war risk premiums for the Persian Gulf have spiked by 600%.

For a standard Very Large Crude Carrier (VLCC) carrying two million barrels, the insurance cost per transit has risen from roughly $30,000 to over $180,000. When combined with the $2 million "protection toll" demanded by Iranian authorities for safe passage—a fee the U.S. Treasury classifies as sanctions evasion—the operational cost of a single voyage now exceeds the profit margin of the cargo itself for all but the most desperate spot-market buyers.

2. The Operational Failure of Alternative Routing

A common fallacy in generalist reporting is the assumption that pipelines can mitigate a Hormuz closure. The data refutes this. The combined capacity of the East-West Pipeline (Saudi Arabia) and the Abu Dhabi Crude Oil Pipeline (UAE) is approximately 6.5 million b/d.

This leaves a systemic deficit of roughly 14 million b/d that cannot be rerouted. The physical reality of global energy geography dictates that 20% of global petroleum liquids consumption is hard-wired to this 33-kilometer-wide chokepoint. The current "dual blockade" has effectively stranded 15% of the world's daily oil supply and 20% of global Liquefied Natural Gas (LNG) exports, specifically impacting QatarEnergy, which has been forced to declare force majeure on nearly all shipments to the European and Asian markets.

3. The Kinetic Deterrence Gap

The Trump administration’s strategy assumed that a naval blockade of Iranian ports would force a reopening of the Strait. Instead, it created a "Dead Zone" in the Gulf of Oman. Iran’s use of shore-to-ship missiles and swarm drone tactics from the Musandam Peninsula has made the 3.2-kilometer-wide shipping lanes untenable for commercial traffic, regardless of U.S. Navy presence. The U.S. military’s inability to "clear" the Strait via airstrikes highlights a fundamental shift in naval warfare: the cost of defending a tanker ($2 million per interceptor missile) is exponentially higher than the cost of the threat ($20,000 loitering munition).

Global Macroeconomic Contagion Functions

The crisis is propagating through the global economy via two primary cost functions: input inflation and caloric insecurity.

The Energy-Inflation Correlation

Brent Crude’s surge past $120 per barrel in March 2026 was not a speculative peak but a reflection of physical scarcity. Unlike the 2022 energy shock, which was a price-access crisis, the 2026 crisis is a physical-availability crisis.

- The European Liquidity Crunch: With gas storage levels at 30% following the 2025-2026 winter, the loss of Qatari LNG has doubled Dutch TTF gas benchmarks.

- The Asian Import Trap: China, India, Japan, and South Korea account for 75% of the oil transiting Hormuz. While China has utilized its 1.4 billion-barrel strategic reserve to buffer the shock, India’s lower reserve-to-consumption ratio has forced an immediate 40% hike in domestic fuel prices, triggering a cooling of the manufacturing sector.

The Caloric Emergency in the GCC

The Gulf Cooperation Council (GCC) states face a unique paradox: they sit on the world’s largest energy reserves but rely on the Strait for 80% of their food imports. The blockade has disrupted 70% of regional food inflows. The shift to air-lifting staples has resulted in food price inflation ranging from 40% to 120% in Bahrain and the UAE. This illustrates the fragility of the "rentier state" model when maritime supply lines are severed.

Strategic Shift: The Rise of the Americas and the Electrostate

The blockade is accelerating a permanent reconfiguration of the global energy order. This transition is characterized by two diverging strategies.

The American Export Surge

U.S. crude exports have climbed to a record 5.2 million b/d. Washington is no longer just a consumer; it is the primary beneficiary of the Middle Eastern supply vacuum. This creates a geopolitical friction point: the U.S. is incentivized to maintain high global prices to support its domestic shale industry, even as its blockade of Iran exacerbates the global shortage.

The Chinese Solar Buffer

China’s response to the crisis has been a radical acceleration of its "Electrostate" transition. By surpassing its 2025 EV targets—with EVs now making up 50% of new car sales—China has reduced its oil import dependency at a rate equivalent to its pre-crisis imports from Saudi Arabia. The blockade has proven that energy security is no longer found in securing sea lanes, but in domesticating the entire energy value chain through renewables and battery storage.

Technical Constraints and Forecasts

Any resolution to the crisis faces significant technical hurdles. Even if a ceasefire were signed tomorrow, the "reopening" of the Strait would be a multi-month process.

- Minesweeping Operations: The suspected deployment of bottom-dwelling naval mines by IRGC forces requires slow, methodical clearance that cannot be performed under the threat of shore-based artillery.

- Vessel Backlog: Over 100 tankers are currently idling in the Indian Ocean and the Persian Gulf. Managing the reintegration of this fleet into global schedules will take a minimum of 90 days.

- Refinery Recalibration: Many Asian refineries are calibrated specifically for the "sour" crudes of the Persian Gulf. The shift to "sweet" Atlantic crudes during the blockade has caused operational wear that will require maintenance shutdowns before a return to full capacity.

The strategic play for industrial consumers is no longer "waiting for the reopening." It is the aggressive decoupling from Middle Eastern energy transit. Logistics firms must shift from a "Lease and Transit" model to a "Reserve and Reshore" model. The Strait of Hormuz has transitioned from a managed risk to a permanent systemic volatility factor. Organizations should prioritize investments in energy-dense storage and alternative Atlantic-basin supply contracts, as the era of cheap, reliable transit through the Persian Gulf has concluded.