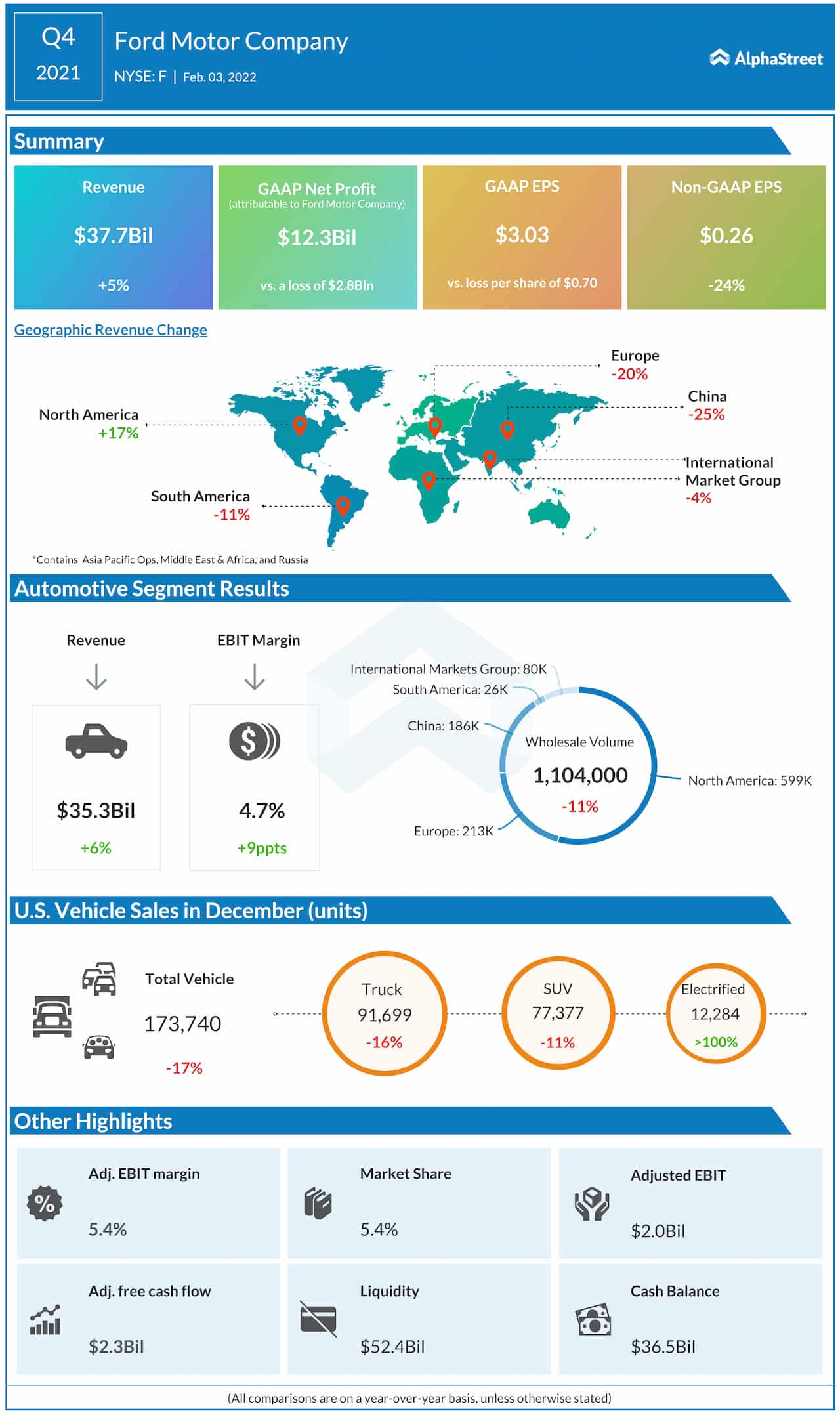

Ford Motor Company’s recent quarterly performance is not merely a failure of volume but a systemic breakdown in the synchronization between legacy internal combustion engine (ICE) profitability and the capital-intensive scaling of the Model e electric vehicle division. The reported earnings miss—the most significant in a 48-month window—reveals a widening delta between the company’s "Ford Pro" commercial success and the persistent margin erosion within its consumer EV segment. To understand the 2026 guidance upgrade, one must first deconstruct the three-way internal friction currently defining the Ford balance sheet.

The Tri-Divisional Friction Model

Ford’s operational structure is currently split into three distinct entities: Ford Blue (ICE and Hybrid), Ford Pro (Commercial and Software), and Ford e (Electric). The earnings miss was driven by a specific failure in the Cost-to-Revenue Ratio within Ford e, where massive R&D and tooling expenditures are hitting the P&L faster than consumer adoption can amortize them.

- Ford Blue Margin Decay: While the ICE business remains the primary cash engine, increased labor costs following the UAW contract negotiations and rising material inputs have compressed the margins that traditionally subsidize EV development.

- Ford Pro’s Sustained Dominance: The commercial sector represents the only segment where software-as-a-service (SaaS) and telematics are successfully creating high-margin recurring revenue. The miss indicates that even these record-setting commercial profits could not offset the losses elsewhere.

- Model e’s Negative Contribution Margin: Every electric vehicle sold currently carries a negative margin when accounting for the fixed costs of battery plant construction and software architecture development.

The Pricing Power Paradox

The primary mechanism behind the earnings shortfall is the collapse of "Pricing Power." During the 2022-2023 period, supply chain constraints allowed Ford to maintain high MSRPs and low incentives. As inventory levels normalized across the industry in late 2024 and 2025, the market shifted from a supply-constrained environment to a demand-constrained environment.

Ford’s inability to maintain its projected "Price Realization" figures stems from a broader macroeconomic cooling. When interest rates remain elevated, the monthly payment on a $60,000 F-150 Lightning becomes prohibitive for the mass-market consumer. To move metal, Ford was forced to increase variable marketing expenses (incentives), which directly cannibalized the quarterly bottom line. This is not a brand failure but a Macroeconomic Interest Rate Sensitivity issue that disproportionately affects high-ticket durable goods.

The Warranty and Quality Bottleneck

A critical, often overlooked factor in Ford’s quarterly miss is the "Warranty Expense Variable." Historically, Ford has struggled with higher-than-average warranty claims relative to its peers, particularly in its initial launches of new powertrain architectures.

The cost of "remanufacturing" or repairing vehicles post-sale acts as a direct drag on the Gross Corporate Margin. In this specific quarter, the "Quality Delta"—the difference between projected and actual repair costs—widened. Until Ford stabilizes its "Initial Quality Study" (IQS) metrics, the leakage of capital through service and recall channels will continue to undermine the gains made in manufacturing efficiency.

Deconstructing the 2026 Guidance Pivot

The decision to guide for a stronger 2026 despite a disastrous Q4 is predicated on the Product Lifecycle Inflection Point. Strategy consultants look for the moment when capital expenditures (CapEx) begin to decline while production volume scales. Ford is betting that 2026 will be that moment for three reasons:

- Gen-2 EV Architecture: Current EV losses are tied to "Gen-1" platforms which were largely adaptations of existing ICE frames. The 2026 models utilize a "Clean Sheet" architecture designed for radical manufacturing simplicity, aiming to reduce parts count by 20-30%.

- Vertical Battery Integration: The "BlueOval SK" battery plants are scheduled to reach peak efficiency by mid-2026. This shifts the cost of batteries from an external procurement expense to an internal manufacturing cost, capturing the margin previously lost to suppliers.

- Hybridization as a Margin Bridge: Recognizing the slowing pace of EV adoption, Ford is pivoting to "Hybrid-First" for its Ford Blue division. Hybrids offer a higher margin profile than EVs while satisfying increasingly stringent EPA fleet emissions standards.

The Inventory Velocity Calculation

The miss was exacerbated by a "Days’ Supply" imbalance. When vehicles sit on dealer lots for more than 60 days, the "Floorplan Interest" and depreciation start to erode the manufacturer's eventual take. Ford ended the quarter with an inventory velocity that was slower than the industry average, forcing a "production trim"—effectively shutting down lines to prevent oversupply. While this preserves long-term brand equity by preventing fire-sale pricing, it results in massive "Under-Absorption" of fixed plant costs in the short term.

The Software-Defined Vehicle (SDV) Revenue Gap

A fundamental pillar of Ford’s long-term strategy is the transition to a software-defined vehicle where features (BlueCruise, Pro-Power Onboard) are sold via subscription. The earnings miss highlights a Temporal Mismatch: Ford is spending billions on the "Digital Backbone" today, but the "Attachment Rate"—the percentage of customers paying for subscriptions—is not yet high enough to impact the EPS (Earnings Per Share).

The 2026 bull case relies on the "Installed Base" reaching a critical mass. By 2026, Ford expects millions of connected vehicles to be on the road, creating a "Flywheel Effect" where low-overhead software revenue begins to pad the thin hardware margins.

Operational Constraints and Labor Dynamics

The structural shift in labor costs cannot be ignored. The post-strike environment has introduced a permanent step-function increase in the Cost of Goods Sold (COGS). To offset this, Ford must find equivalent "Operational Efficiencies" through automation or supply chain consolidation. The quarterly miss proves that these efficiencies have not yet materialized at a scale sufficient to neutralize the labor hike.

Strategic Execution Path

To realize the 2026 projections, the executive team must execute a "Dual-Track Rationalization":

- Aggressive ICE Platform Consolidation: Reducing the number of unique chassis and engine combinations in the Ford Blue portfolio to maximize "Economies of Scale" in a shrinking segment.

- Model e Capital Discipline: Shifting from a "Growth at All Costs" EV strategy to a "Value-Focused" deployment, where production is strictly tied to demand signals rather than optimistic forecast models.

The path to 2026 is not a straight line of recovery but a volatile transition from a hardware-centric manufacturing firm to an integrated energy and software entity. The quarterly miss is the "J-Curve" effect in practice: a necessary dip in performance as the company retools its entire fundamental logic. Investors and analysts must monitor the "Contribution Margin per Unit" in the EV space; if this remains negative by mid-2025, the 2026 guidance becomes mathematically untenable.

The most effective move for the next 18 months is a ruthless prioritization of the Ford Pro segment. By leveraging the commercial division’s data-rich environment to test new software architectures before they hit the more volatile consumer market, Ford can "De-Risk" its digital transition. Success in 2026 will be determined by whether Ford can turn its trucks into mobile offices that command a premium, rather than just commodities that compete on price.